Housing affordability has become the domestic fixation in Washington this year. Most recently, the White House signed an executive order aimed at limiting large institutional investors—Wall Street firms—from purchasing single-family homes. The intent is straightforward: reduce competition for first-time homebuyers competing in the same market.

That proposal is only one piece of a growing list. Other ideas floated in recent weeks include extended mortgage terms and so-called “portable mortgages,” which would allow buyers to carry favorable loan terms from one home to the next. None of these proposals exist in a vacuum. In housing, for every intended winner, there is almost always an unintended loser.

Consider the push to “fix” affordability by lowering home prices. That sounds good—until you remember who already owns the homes. Roughly 88 million U.S. households are homeowners today. Housing is the largest asset most families will ever hold. According to the Federal Reserve, that collective housing equity totals nearly $35 trillion as of the third quarter of 2025. Policies that materially reduce home values don’t just hit investors—they hit everyday households, retirement plans, and long-term financial stability.

So what would it actually take to return affordability to pre-pandemic levels—think 2019?

An analysis from Realtor.com defines affordability as a buyer spending 20% of their monthly income on principal and interest. Under that framework, one of three things must happen:

First, if home prices and mortgage rates stay where they are today, median household income would need to rise 56%, to roughly $123,000. Wages are rising faster than home prices—but at the current pace, that adjustment would take close to a decade.

Second, mortgage rates would need to fall to 2.65% to restore the same purchasing power buyers had in 2019. That scenario is, realistically, off the table.

Third, home prices could decline—but they would need to fall by 35% nationwide to make the math work. That level of correction would be economically and politically destabilizing.

And yet, an even bigger problem looms over all three scenarios: supply.

Even if rates fall, there simply aren’t enough homes. Builders remain cautious, not because they don’t want to build, but because construction costs—labor, materials, financing—have risen dramatically. Most economists agree on this point: without materially increasing housing supply, demand-side policy tweaks will not solve affordability. That’s the missing piece in most current federal proposals—and it’s the one that actually matters.

Here’s my blunt take. Rates are roughly where they should be. They are not going back to 3%. Housing affordability, as many define it, isn’t meaningfully improving because prices are effectively stuck. What does need to change is expectation.

That’s why the average first-time homebuyer is now around 40 years old and first-time buyers made up just 21% of homebuying. Household income assumptions have shifted as well—it’s no longer one income buying a home, but often two working adults. Capitalism works when supply and demand are allowed to function together. When policy focuses almost exclusively on stimulating demand—without addressing supply—we don’t fix housing. We simply reshuffle who gets left behind.

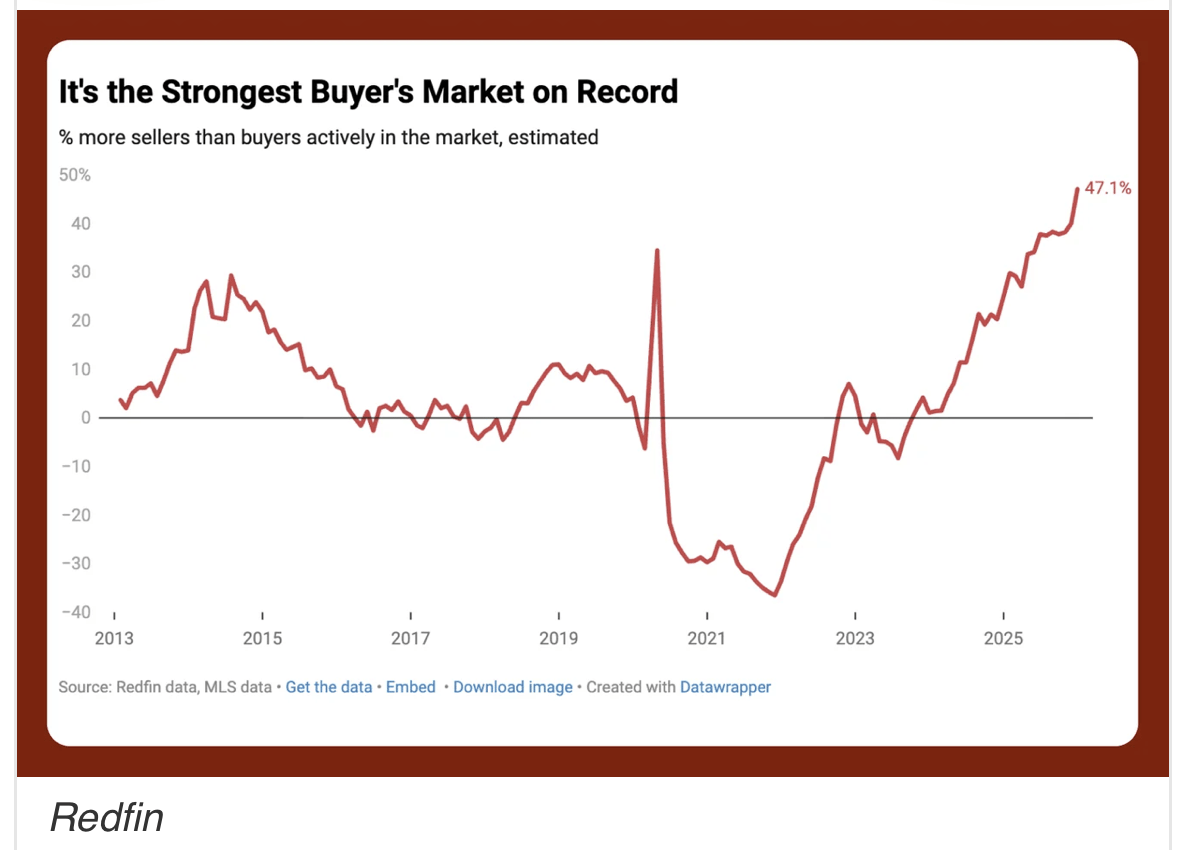

📸: The strongest buyer’s market in over a decade—on paper. Redfin reports 47.1% more sellers than buyers in December, the biggest gap since 2013. Sounds bullish for buyers… except contracts fell nearly 10% month-over-month. Why? Inventory (or lack of it). Buyers are waiting for real choice before making big moves—but supply is still tight. Add rates to the mix: mortgage rates have stayed above 6% for more than three years, and for the first time since 2021, more Americans now have rates above 6% than below 3%. Still, nearly half of all mortgages sit under 4%, keeping many homeowners locked in and hesitant to move. But life doesn’t pause. Jobs change. People marry, divorce, grow families, retire, and chase better lifestyles—and that’s finally starting to crack the lock-in effect. Meanwhile, consumer confidence just hit a decade low, falling below economists’ expectations. Translation: the market wants to move… it’s just Isn't (yet).